2026 looks like a good year to buy property in Switzerland. With the SNB holding rates at 0%, the mortgage rates are low, rents are high, and the numbers increasingly favour ownership.

In many cases, that’s true. But that’s not actually the interesting part.

The interesting question is whether the answer depends on where in Switzerland you live?

Here’s what the market looks like today for a 4.5-room apartment:

| City | Purchase Price Range (CHF) | Monthly Rent Range (CHF) |

| Zurich | 1,800,000 – 2,400,000 | 4,500 – 6,000 |

| Geneva | 1,800,000 – 2,300,000 | 4,500 – 6,000 |

| Basel | 1,150,000 – 1,550,000 | 3,500 – 4,500 |

| Bern | 1,050,000 – 1,350,000 | 3,200 – 4,200 |

| Lugano | 900,000 – 1,300,000 | 2,800 – 3,800 |

Source: Personal research conducted in March 2026 based on active listings from major Swiss property portals (e.g., Homegate, ImmoScout24, and Comparis)

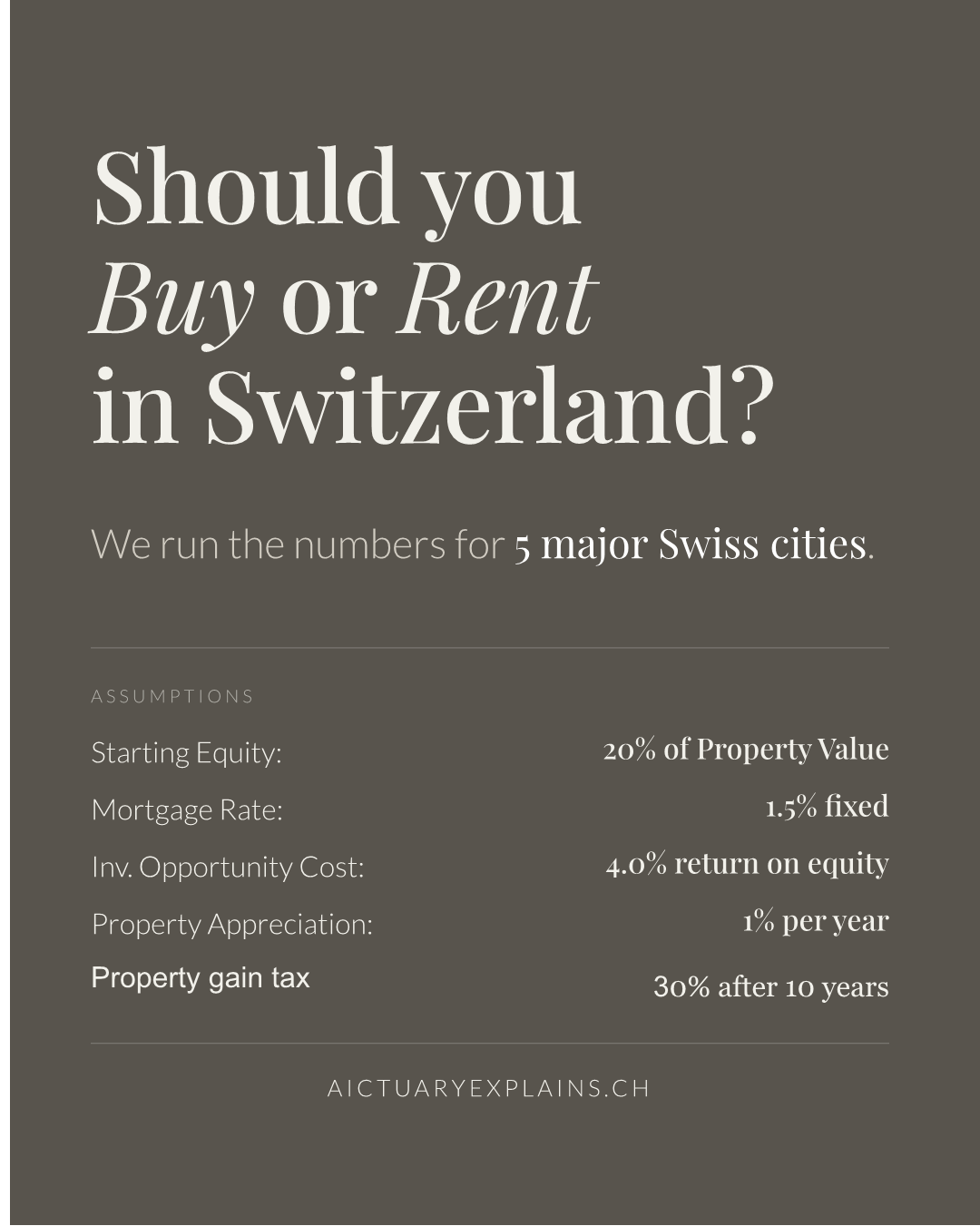

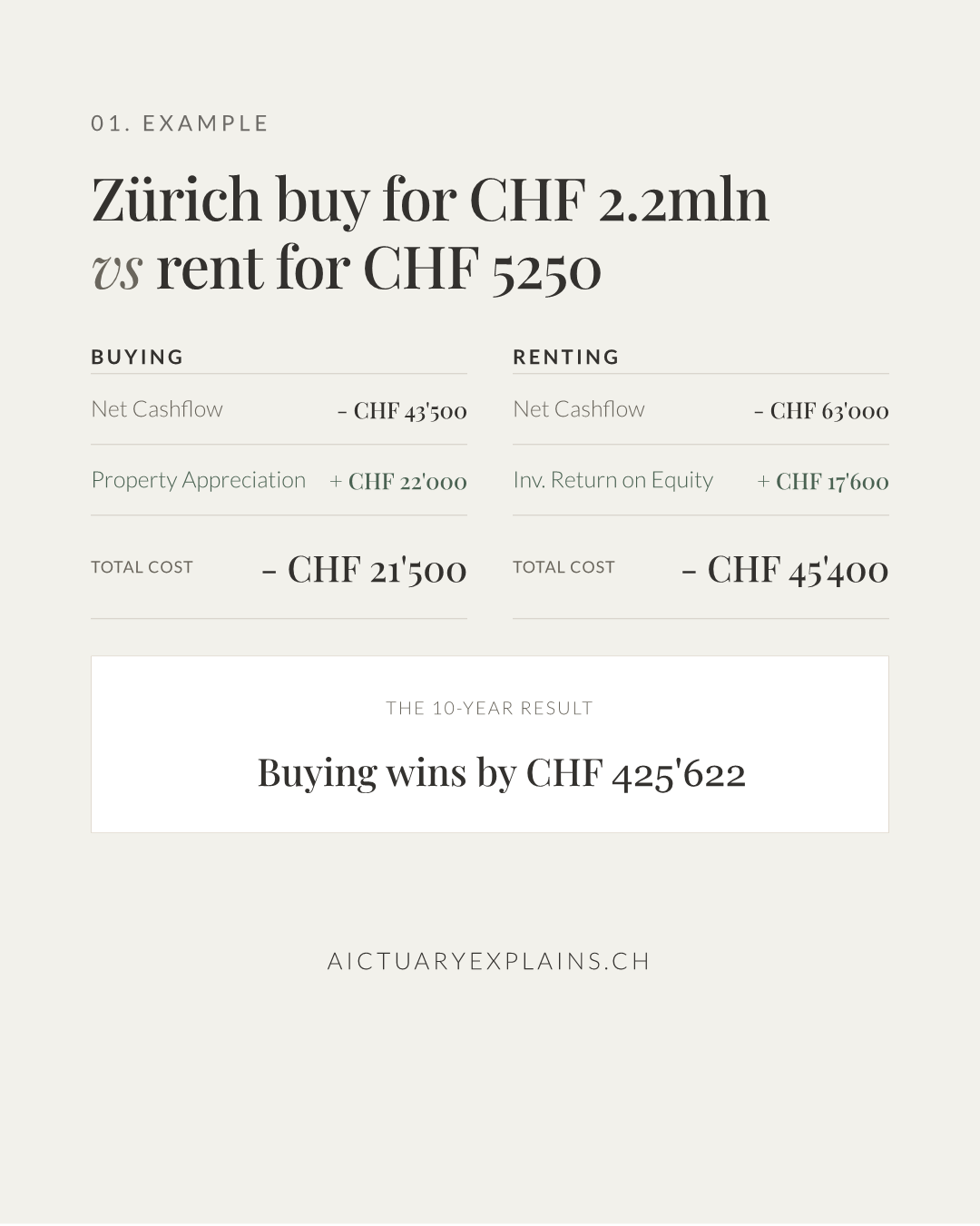

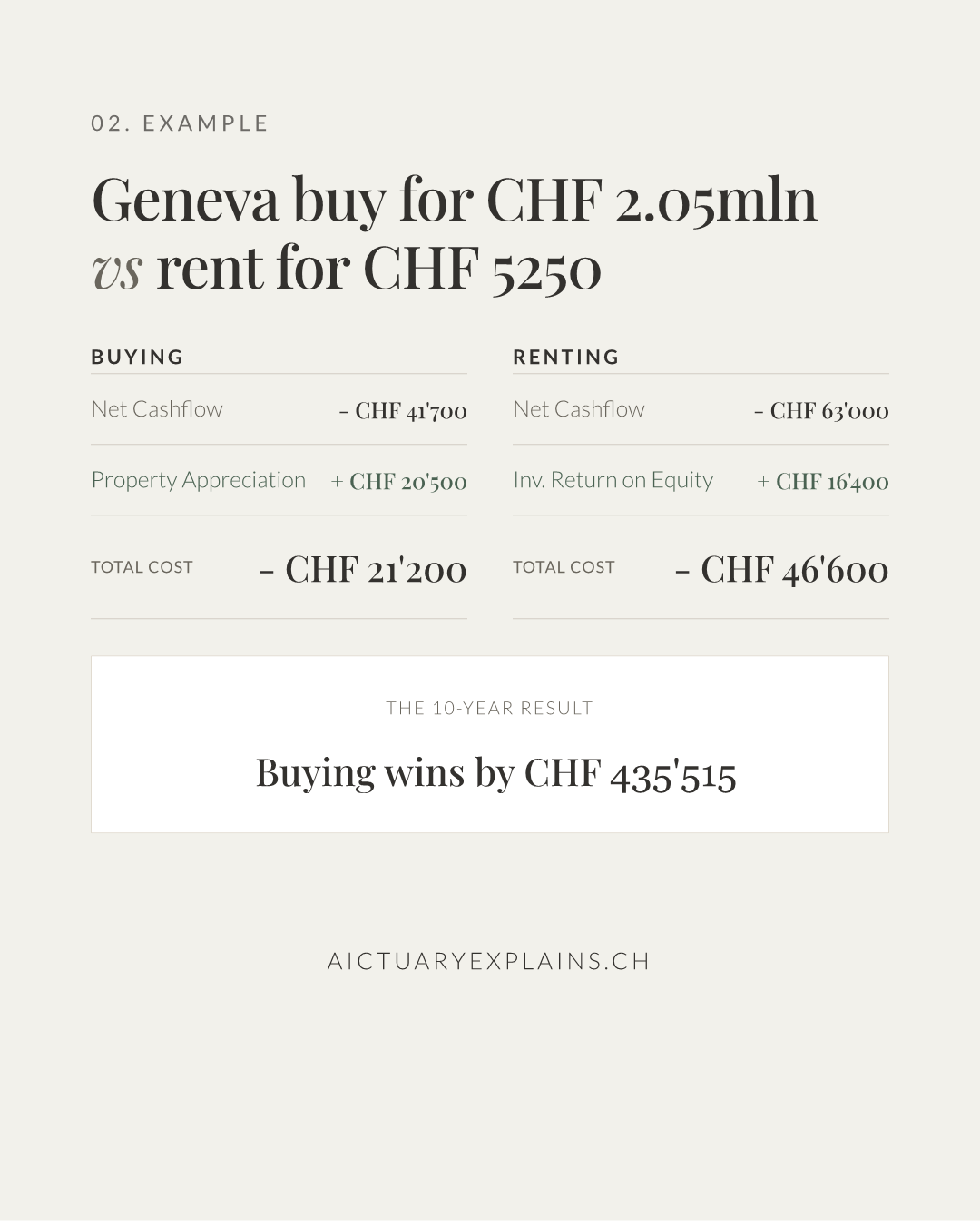

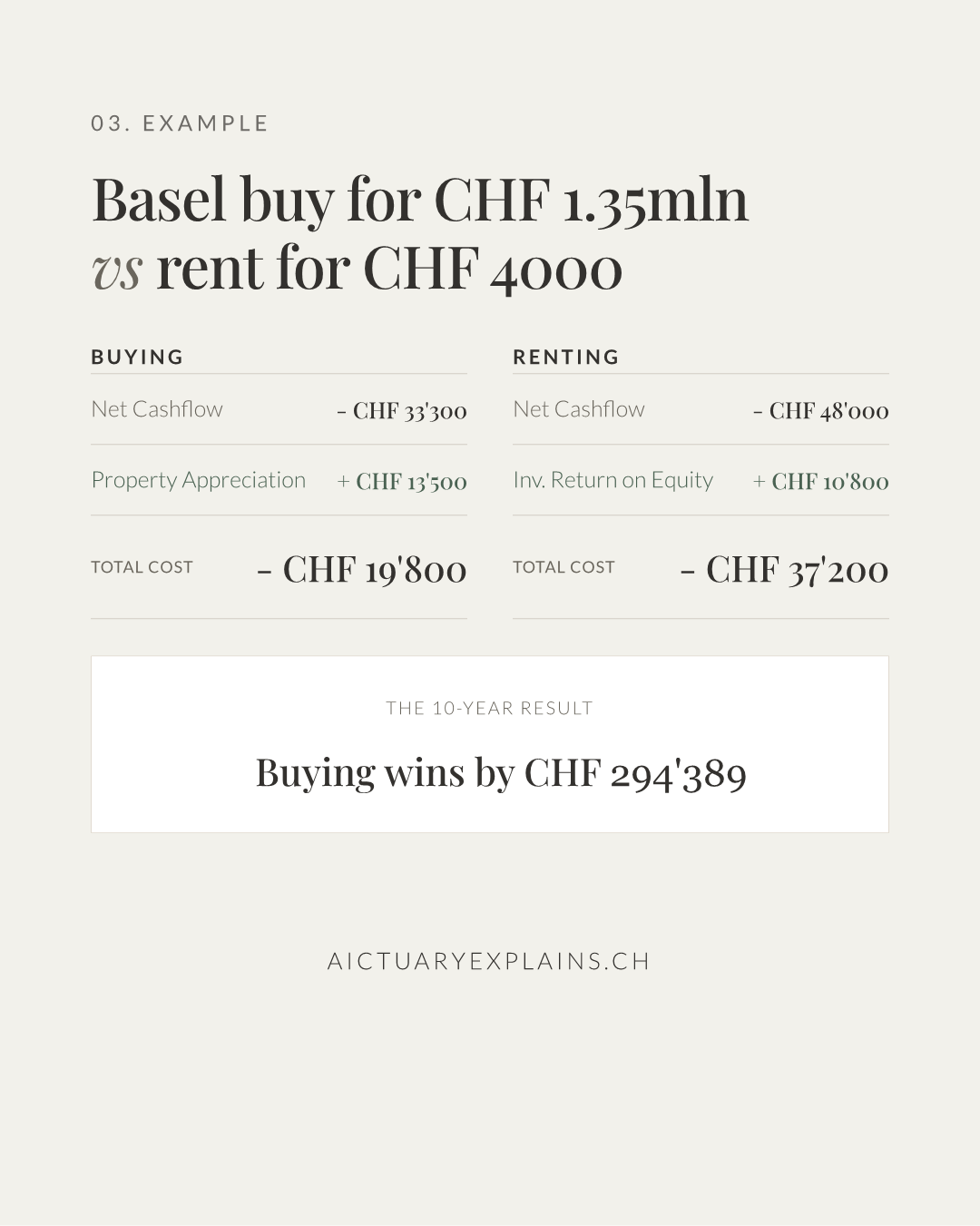

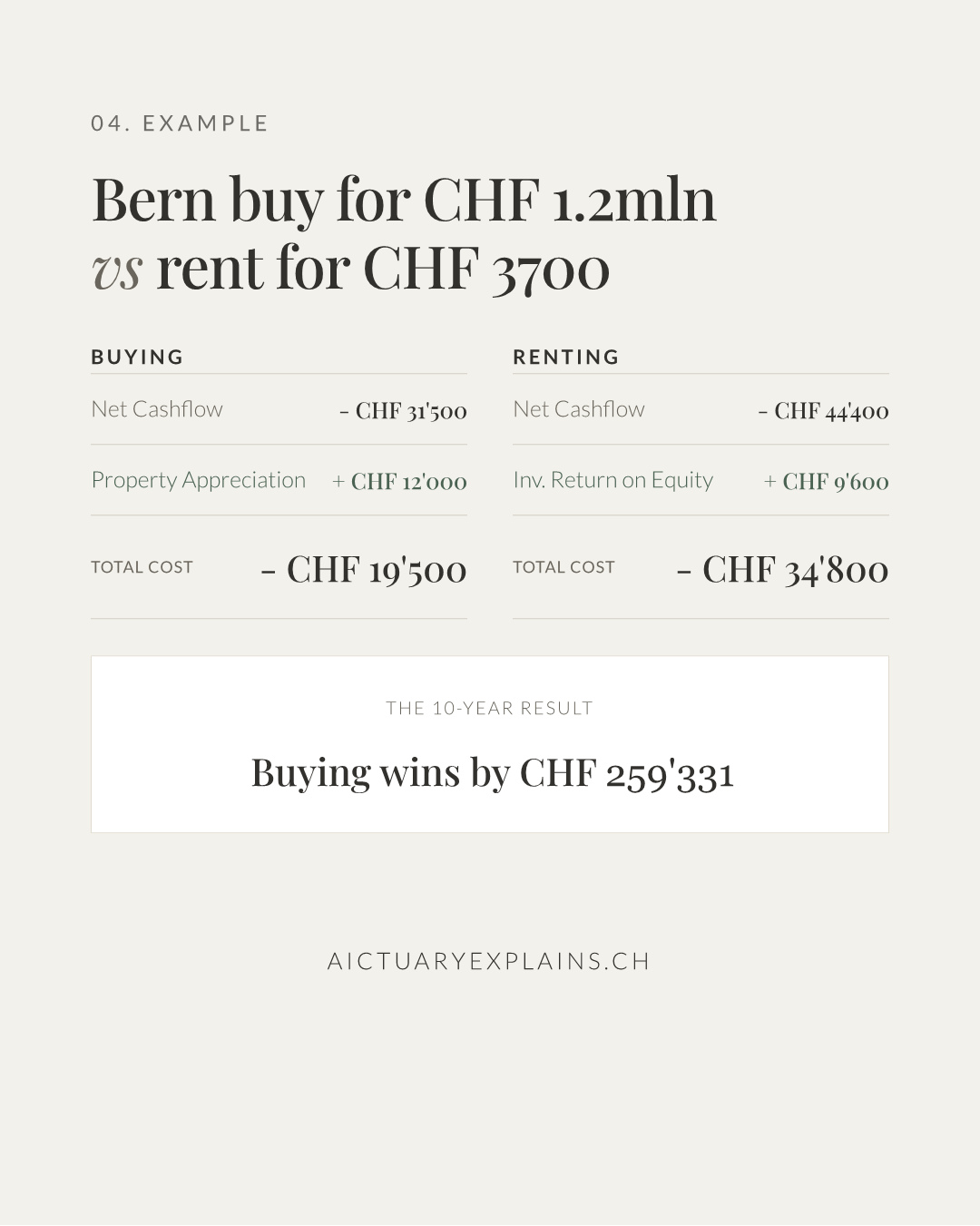

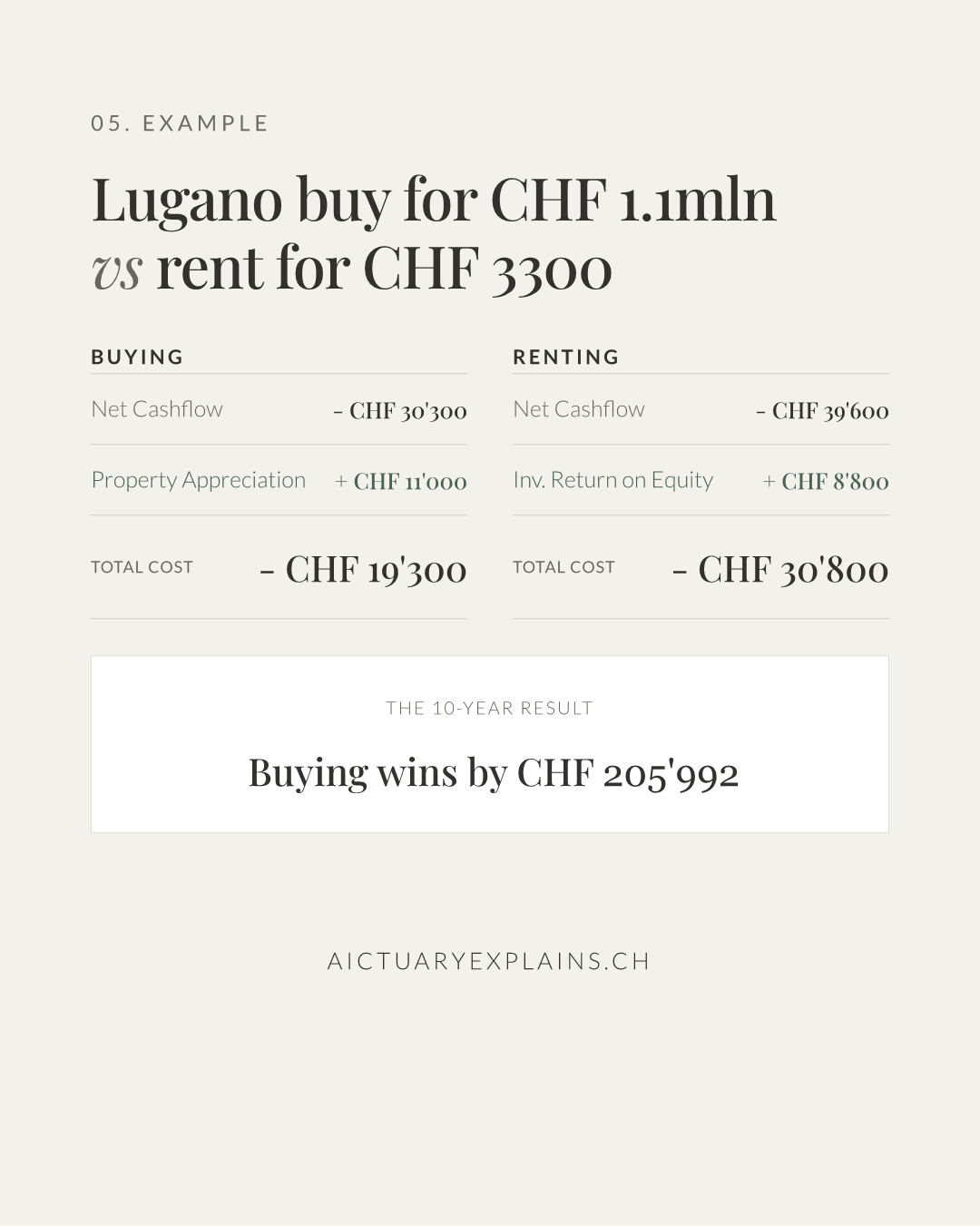

I ran all five cities through my buy vs rent calculator. It covers the details that matter in Switzerland: realistic maintenance costs, property gains tax and opportunity cost. I assumed mid range purchase price and mid range rent for each city.

If you’re curious how the results compare across cities, I’ve put it into a short carousel.

However calculations can change quickly if you have an old rent – it’s essentially a hidden asset class. You can test your specific scenario here:

Whether 2026 is truly the ‘best’ year to buy property in Switzerland is a question only your own numbers can answer. I’ve been looking closely at how the math has shifted since the high-interest years of 2022–2024, and the change is significant. Here is the reality I’m seeing in the data right now:

- The Return of 0% Rates: With the SNB holding policy rates at 0%, the cost of money is back to historical lows. Compared to 2024, when 10-year fixed mortgages were around 2.5%–3%, your monthly interest burden in 2026 has effectively been halfed.

- The Rental Squeeze: While mortgage costs dropped, rents didn’t. In cities like Zurich and Geneva, the supply shortage has pushed rents up by 15–20% over the last three years.

If you want to understand why the numbers often tip in favor of owners over time, I’ve broken down the ‘wealth effect’ in this post.

This article is a part a blog series on homeownership in Switzerland. Each post is a simplified, standalone piece drawn from my upcoming book Homeownership in Switzerland: How to Buy, Finance and Invest in Swiss Real Estate, which looks at the topic holistically.

See you soon in the next article on opportunity cost.

Frequently Asked Questions

1. Is it better to buy now or wait for property prices to drop further?

While nobody can perfectly time the market, waiting for a significant price drop in Switzerland is a risky strategy. Historically, Swiss property prices are extremely resilient due to low vacancy rates and limited supply. Often, the money you “save” by waiting for a price drop is offset by the property prices appreciation in the meantime. If you have a specific scenario in mind, feel free to ask AIctuary. I’ve built this AI assistant to provide precise answers based on my actuarial frameworks and the latest Swiss financial regulations.

2. Can I use my 2nd Pillar (Pensionskasse) to buy a home?

Yes, you can either withdraw the funds or pledge them (Verpfändung). Withdrawing increases your equity and lowers your monthly interest, but it reduces your future retirement benefits. Pledging keeps your pension intact but requires a higher mortgage. I explained the details of using 2nd Pillar to buy a home in this post: How to Use Your Pension to Buy a Home in Switzerland (Pillar 2 Withdrawal Explained).

3. Is it true I can repay my mortgage more efficiently using my pension (Pillar 2)?

Absolutely. Many people make the mistake of repaying their mortgage with “after-tax” money from their bank account. I shared in one of my earlier articles a more tax-optimized approach: the “Smart Mortgage Loop”. Instead of direct repayment, you can make voluntary buy-ins to your Pillar 2 (Pensionskasse), which are fully tax-deductible. You then use the Home Ownership Promotion (WEF) rules to withdraw those funds to reduce your mortgage. This effectively allows you to pay down your debt using “tax-free” money, significantly accelerating your path to being debt-free. You can see a concrete example of this strategy here.

I don’t publish often. Only when I believe something is truly worth sharing. If you’d like the next guide when it’s ready, you’re welcome to join below:

Send me the next guide