Is buying a home better than renting in Switzerland?

Sometimes it is.

Sometimes it isn’t.

The answer depends entirely on your numbers. And not just one or two of them, but a small handful of factors that need to be modelled together. When people argue endlessly about rent versus buy, they usually talk past each other because they are implicitly using different assumptions.

This post gives you a simple framework to work out which side you’re actually on.

Ultimately, you’ll want to run your own numbers. The outcome depends on things that are very personal: what you currently pay in rent, what kind of property you would realistically buy instead, how much equity you have, and how your financing is structured. That’s exactly why I built an interactive buy-vs-rent calculator that compares renting and owning on a like-for-like basis, including taxes, mortgage costs and opportunity cost.

But before you plug in your own situation, let’s look at a clean baseline example.

Numbers first: the Zurich Scenario

Let’s set up a fair comparison. To keep this grounded, I’ll use realistic Zurich numbers for 2026 and be transparent about every assumption.

The property: imagine a 4.5-room apartment in Zurich-Oerlikon.

About 120 m², built in 1990, with underground parking. It’s not new, but it’s in good shape and doesn’t require major renovation.

The purchase price is CHF 1.5 million.

The buyer has CHF 300 000 in available equity.

Now consider the alternative. Renting a comparable apartment in the same area currently costs around CHF 3 500 per month. Add roughly CHF 300 per month in Nebenkosten and the annual rent comes to CHF 45 600.

Now let’s see what buying the same apartment actually costs.

Buying: the Real Annual Cost

When you buy a home in Switzerland, your costs spread across several categories. Let me walk you through each one.

Mortgage

With CHF 300 000 in equity, the mortgage amounts to CHF 1.2 million. At an interest rate of 1.5 percent, the annual interest payment is about CHF 18 000. This is the real interest you pay which is not the hypothetical 5 percent rate banks use in affordability calculations. That higher rate is a stress test, not an expense that shows up on your bank statement.

Nebenkosten and renovation fund

As an owner, you still pay Nebenkosten, which we can assume are similar to renting at around CHF 300 per month. Because the building is older, it’s also reasonable to assume a higher contribution to the building’s maintenance and renovation fund, say CHF 500 per month. Together, those costs add up to CHF 9 600 per year.

Your own maintenance reserve

Then there’s maintenance inside your own apartment. Banks typically assume 1% of the property value per year, which would be CHF 15 000 for this apartment. But that figure includes major renovations like kitchens and bathrooms spread over decades. But if you rent, your landlord won’t spend CHF 15 0000 every year. For a 1990s apartment in decent condition, assuming around half of that, roughly CHF 7 500 per year, is a much fairer comparison with renting. It covers normal wear and tear: small repairs, appliances, repainting, the unglamorous but inevitable stuff.

Mandatory amortisation

Swiss rules require you to reduce the mortgage to 65 percent of the property value within 15 years. In this case, that means paying back CHF 225 000, or about CHF 15 000 per year.

This is where many comparisons go off the rails. That CHF 15 000 is not an economic cost. It is forced savings. Yes, the cash leaves your account, but it reappears as equity, typically via Pillar 3a, where it can be invested. It feels like an expense, but it isn’t money disappearing.

And if you rent you probably anyway put 15 000 into 3a Pillar if there’s two of you. So thinking about it as a forced saving provides more fair comparison to renting.

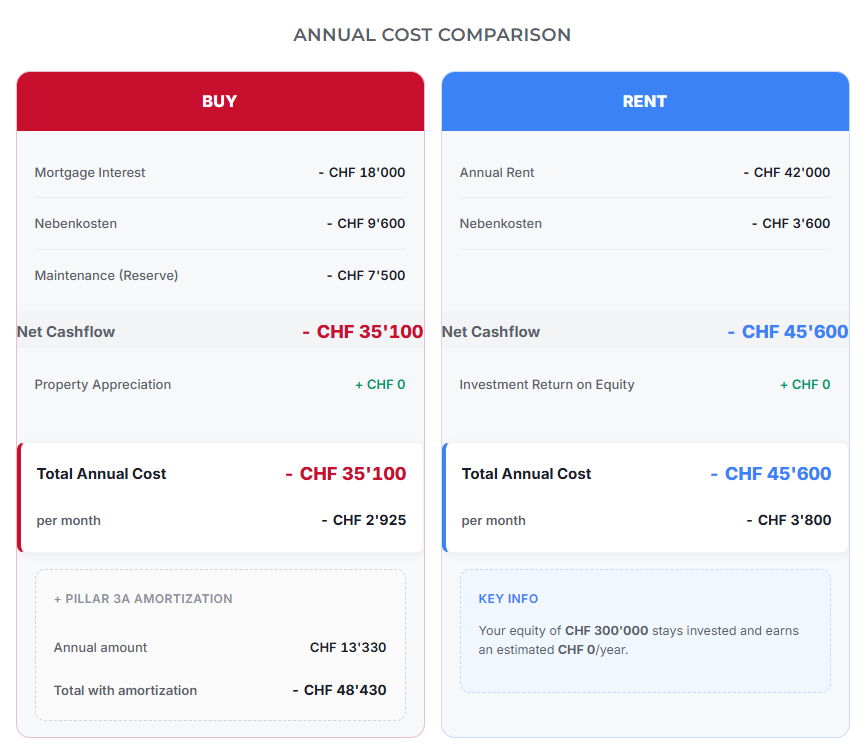

Total Annual Cost of Ownership

If you put everything together, the annual cash flows of ownership look roughly like this. About CHF 18 000 in interest, CHF 9 600 in Nebenkosten and building reserves, and CHF 7 500 as a maintenance buffer. That comes to around CHF 35 100 per year in actual running costs.

Total Annual Cost of Ownership = CHF 35 100

On top of that sits the CHF 15 000 of amortisation, which is savings.

Rent vs Buy: the Comparison

Renting the equivalent apartment costs CHF 45 600 per year. That’s it. No maintenance reserves. No amortisation. One clean number. But keep in mind: that CHF 45,600 is a hard running cost that leaves your account.

Total Annual Cost of Renting = CHF 45 600

Compared to that, owning the apartment comes with annual running costs of about CHF 35 100, including a sensible repair buffer. In this scenario, buying is roughly CHF 10 500 per year cheaper than renting.

Buying is CHF 10 500 per year cheaper

This is how the comparison looks in the ActuaryExplains.ch calculator.

To keep things simple, I’ve left out opportunity cost and property price appreciation for now. The focus for now is on annual cost for buy vs rent. Calculator also shows what happens to your net worth over time depending on whether you rent or buy, using consistent assumptions for both paths.

What this tells us?

In this baseline Zurich example, buying clearly wins on cash flow. I’ve run similar comparisons across Switzerland: a CHF 2 million modern flat in Geneva, a much cheaper older apartment in Bern. And the pattern is surprisingly consistent. Buying comes out ahead in most cases if you compare to current market rents and with current interest rates. Sometimes by a wide margin. Sometimes just barely.

In above calculation I assumed a 1.5% mortgage rate, and CHF 3,800 per month in equivalent rent.

Change any of these, and the answer may shift.

But buying wins in most cases under current market conditions, and this is before we factor in one of the most powerful, and most misunderstood, aspects of homeownership: leverage. I’ll come back to that in a future article.

Before that, though, we need to deal with the most common, and entirely valid, counter-arguments to everything you’ve just read.

What about opportunity cost?

What if you have a below-market rental?

Those questions deserve a proper answer.

This article is the first in a blog series on homeownership in Switzerland. Each post is a simplified, standalone piece drawn from my upcoming book Homeownership in Switzerland: How to Buy, Finance and Manage Your Property Without Burnout, which looks at the topic holistically.

See you soon in the next article on opportunity cost.

For homeowners, there is also a lesser-known option to repay part of the mortgage using pre-tax money, which I explain in this article: A Proven Way to Repay Your Mortgage — How to Become Debt-Free in Switzerland.

If Actuary Explains saved you time, money, or simply clarified a complex topic, you can support the blog here:

Thanks for this, the calculator is really helpful. I’ve owned a place in Switzerland for about 2 years and it was reassuring to see it was the right decision.

I’ve done simulations like yours previously in excel spreadsheets and came to the same conclusion. For me buying wins.

Hey iwan, thanks for your nice words! In our case buying was also financially better than renting, even more so when we include opportunity cost. But i will cover it it more details in my next post. See you soon!