Why do homeowners often build wealth much faster than renters?

The answer is leverage.

Leverage is one mathematical advantage of owning property that rarely shows up in simple rent-versus-buy comparisons.

And property is one of the few investments where ordinary people can access leverage without complicated financial instruments.

When people hear the word leverage, they imagine something sophisticated.

It isn’t.

Leverage simply means using other people’s money to control more assets than you could afford on your own.

Property is one of the clearest places to see how it works.

To understand how leverage works in property, it helps to see that it isn’t new.

Leverage Is an Ancient Idea

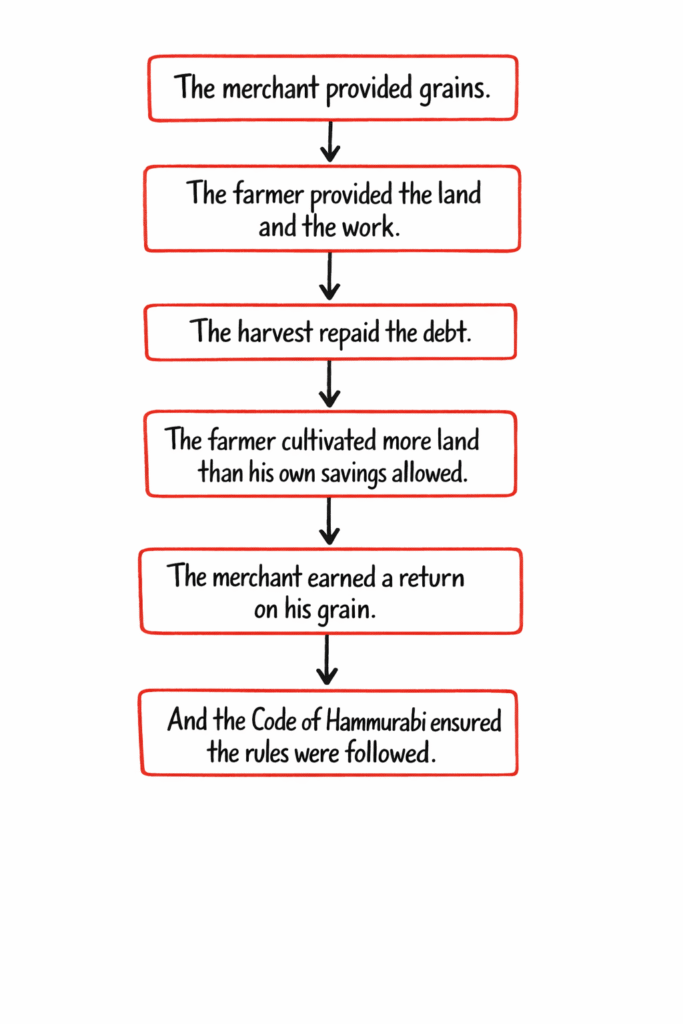

Nearly four thousand years ago, on the fertile land between the Tigris and Euphrates, a Babylonian farmer prepared for planting season.

His field was ready. But farming required more than land.

He needed seeds, tools, maybe an extra ox, and enough grain to feed his family until the harvest months later. The problem was that his income only came once a year, after crops were gathered.

So before the season began, the farmer walked into the nearby town market and met with merchant. The merchant agreed to lend him grain.

With that loan, the farmer could plant his entire field instead of just a small portion. The harvest could now be much larger than what his own grain would have allowed.

But the merchant needed protection. So they wrote a contract. The farmer promised to repay the loan after the harvest, along with an agreed amount of interest (more grain). The loan was secured by the output of the field and by rights tied to the land.

The farmer kept cultivating the land and harvesting the grain.

In modern language, this would look very familiar. The farmer was operating with resources larger than his own wealth — using borrowed capital to produce a bigger harvest. In other words, he was using leverage.

With time the system got regulated and structured carefully under the laws of Hammurabi.

The law also set customary interest rates — 33⅓% for grain loans. Contracts were written on clay tablets and witnessed.

If a storm or flood destroyed the harvest, the law protected the farmer. Repayment could be postponed, and interest for that year was cancelled.

Creditors also had limits. They could not simply seize property or act outside the rules — doing so could lead to legal punishment.

In extreme hardship, a debtor might even deliver a wife/son/daughter to work off a debt. Which means he could pledge labour to repay a debt, but even that arrangement had strict time limits (3 years) written into law.

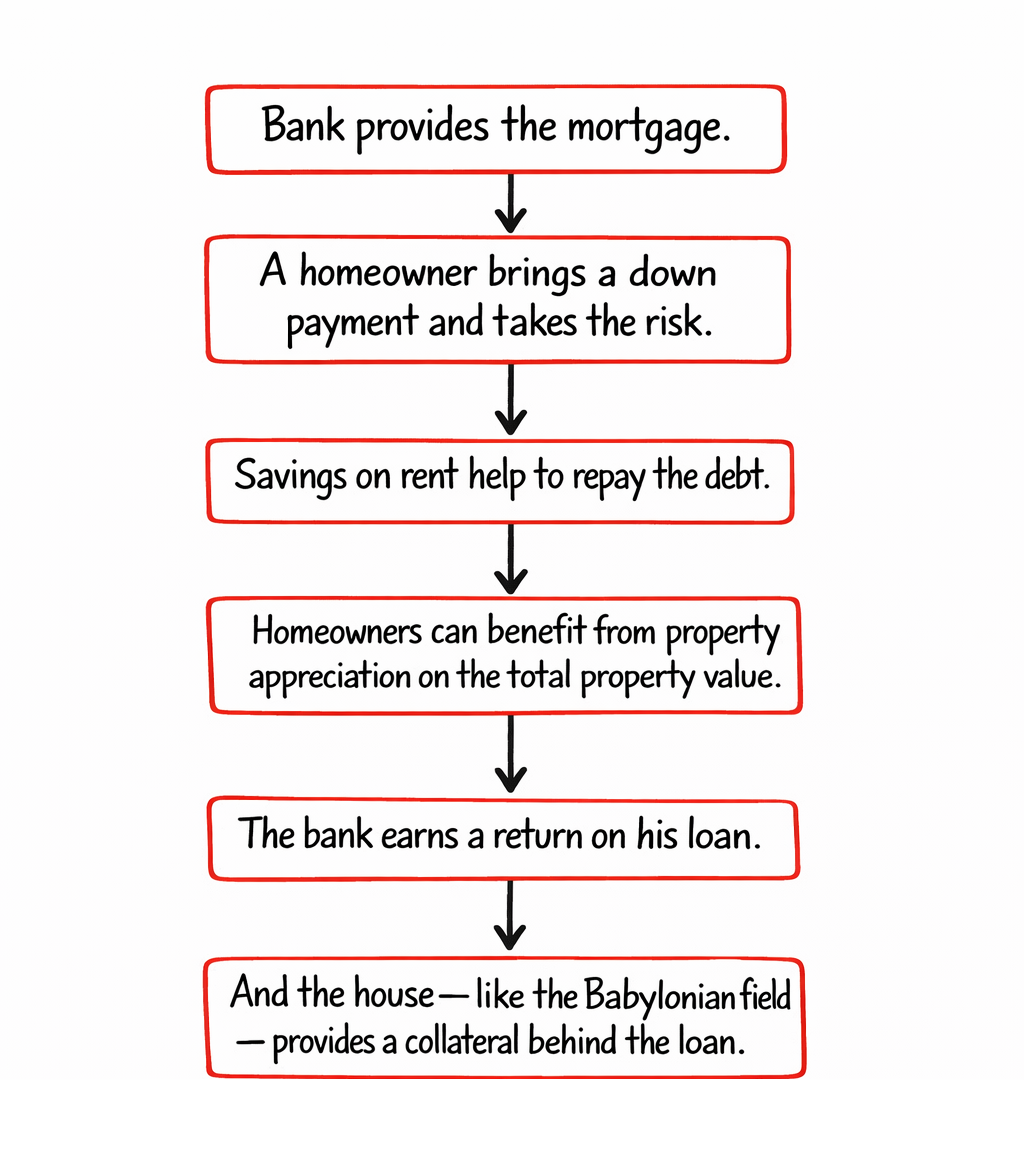

Babylonian structure and modern mortgage structure look suprisingly similar:

What Is Property Leverage?

What can I do with CHF 300,000?

I could keep it in savings. I could invest it in the stock market. Or I could use it as a down payment on a property.

In Switzerland, that CHF 300,000 could allow me to buy a CHF 1.5 million home.

The bank provides the remaining CHF 1.2 million mortgage.

So with CHF 300,000 of my own money, I now control a CHF 1.5 million asset.

That’s 5:1 leverage. I control asset worth 5 times more than my own investment.

I own 100% of the property — even though I only provided 20% of the cash.

Friendly side of Leverage: Why Does Leverage Increase Returns?

Now imagine the property increases in value by 10%.

CHF 1,500,000 → CHF 1,650,000.

The value increased by CHF 150,000.

But remember: my own investment was only CHF 300,000.

So my return isn’t 10%.

It’s 50%.

That’s the part of leverage people love.

That CHF 150,000 is an unrealized gain unless I sell the property.

You generally can’t access this kind of leverage when investing in stocks unless you open margin accounts and accept significant financial risk.

With property, the leverage is simply built into the system. Banks provide it as part of normal mortgage financing.

Terrifying side of Leverage: Why Leverage is Dangerous in Falling Property Markets?

Of course, leverage works both ways.

If property prices fall, the same mathematics applies in reverse.

Imagine the property falls by 10%.

CHF 1,500,000 → CHF 1,350,000.

Your equity was CHF 300,000 → now it’s CHF 150,000.

The asset fell 10% → your equity fell 50%. I now have CHF 150’000 of unrealized loss.

Leverage doesn’t care about direction.

This is why some of the most famous investors have always treated leverage with caution.

“There are only three ways a smart person can go broke: liquor, ladies, and leverage“

– Charlie Munger

In this article, I explain a smart way to deleverage your mortgage using pre-tax money: A Proven Way to Repay Your Mortgage — How to Become Debt-Free in Switzerland.

The Psychology of Leverage

The psychological side of leverage is just as important as the mathematics.

In rising markets, leverage feels like having a helpful friend.

In falling markets, it feels terrifying.

The truth is that leverage itself is neither good nor bad. It’s simply a tool.

Used conservatively on durable assets — like well-located property — it can accelerate wealth over time.

Used aggressively on speculative assets, it can destroy it just as quickly.

This article is the second in a blog series on homeownership in Switzerland. Each post is a simplified, standalone piece drawn from my upcoming book Homeownership in Switzerland: How to Buy, Finance and Manage Your Property Without Burnout, which looks at the topic holistically.

The first article in this blog series is Rent vs Buy in Switzerland: Which Is Better? including an interactive Buy vs Rent calculator.

See you soon in the next article on opportunity cost.

Coming in 2026 Homeownership in Switzerland

I’m writing a book for people who want to understand the Swiss property system before making a million-franc decision

Frequently Asked Questions

1. Is it better to buy now or wait for property prices to drop further?

While nobody can perfectly time the market, waiting for a significant price drop in Switzerland is a risky strategy. Historically, Swiss property prices are extremely resilient due to low vacancy rates and limited supply. Often, the money you “save” by waiting for a price drop is offset by the property prices appreciation in the meantime. If you have a specific scenario in mind, feel free to ask AIctuary. I’ve built this AI assistant to provide precise answers based on my actuarial frameworks and the latest Swiss financial regulations.

2. Can I use my 2nd Pillar (Pensionskasse) to buy a home?

Yes, you can either withdraw the funds or pledge them (Verpfändung). Withdrawing increases your equity and lowers your monthly interest, but it reduces your future retirement benefits. Pledging keeps your pension intact but requires a higher mortgage. I explained the details of using 2nd Pillar to buy a home in this post: How to Use Your Pension to Buy a Home in Switzerland (Pillar 2 Withdrawal Explained).

3. Is it true I can repay my mortgage more efficiently using my pension (Pillar 2)?

Absolutely. Many people make the mistake of repaying their mortgage with “after-tax” money from their bank account. I shared in one of my earlier articles a more tax-optimized approach: the “Smart Mortgage Loop”. Instead of direct repayment, you can make voluntary buy-ins to your Pillar 2 (Pensionskasse), which are fully tax-deductible. You then use the Home Ownership Promotion (WEF) rules to withdraw those funds to reduce your mortgage. This effectively allows you to pay down your debt using “tax-free” money, significantly accelerating your path to being debt-free. You can see a concrete example of this strategy here.

Join 1'400+ readers making smarter Swiss financial decisions:

Send me the next guide