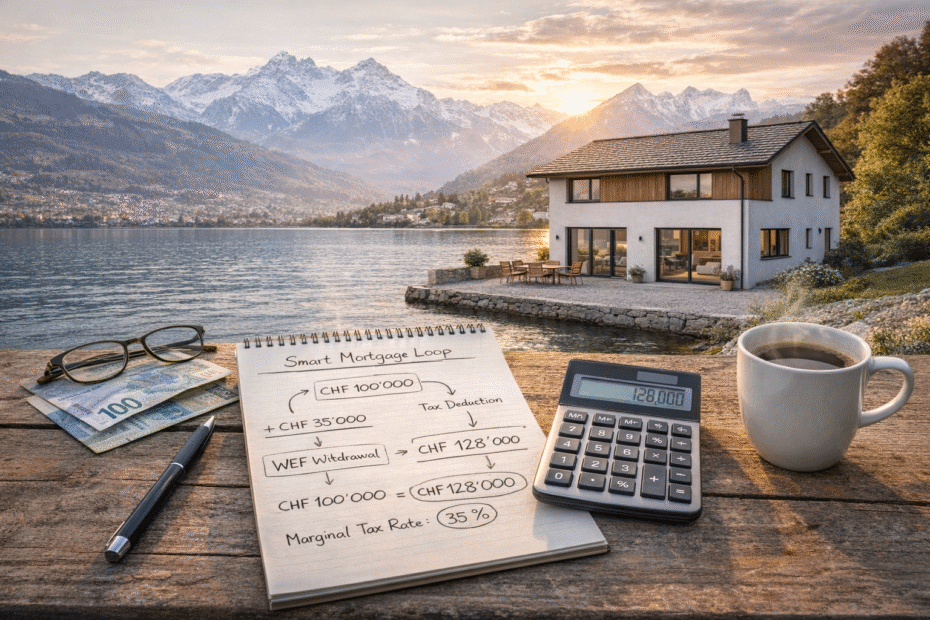

A proven way to repay your mortgage: an example & calculator

A concrete example of how the Swiss pension system can be used to repay a mortgage more efficiently, using Pillar 2 buy-ins and tax optimisation.

A concrete example of how the Swiss pension system can be used to repay a mortgage more efficiently, using Pillar 2 buy-ins and tax optimisation.

Instead of simply repaying your mortgage with after-tax money, you can use your Pillar 2 pension to do it more efficiently — turning one rule (the WEF withdrawal) into a tax-optimized “smart mortgage loop.”

For many families, WEF is the difference between “we’ll buy someday” and “we can actually do this now.”

This guide explains how Swiss Pillar 2 and Pillar 3a can be used to finance your own home — pledge vs withdrawal, real tax rules, limits, and what we learned from using WEF ourselves.

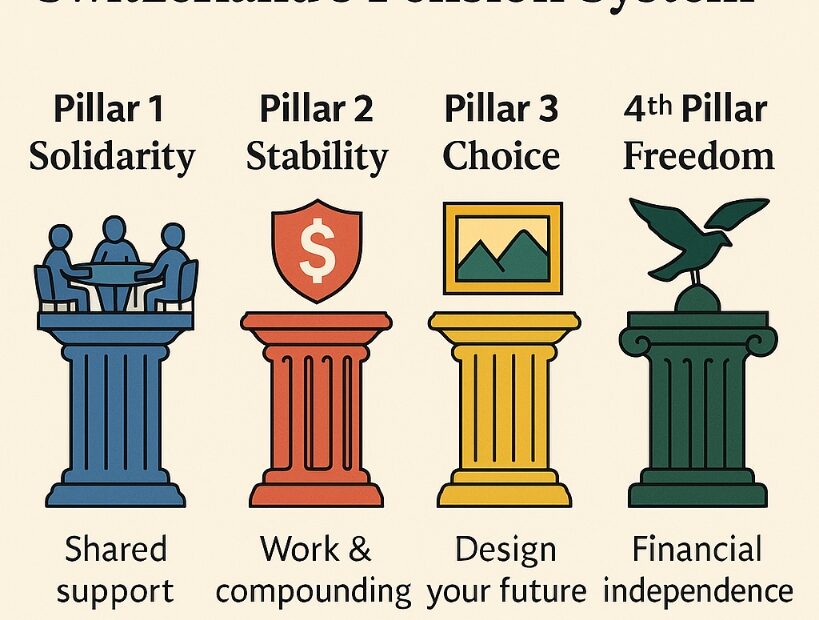

Most people only think about their pension when retirement suddenly feels close — but by then the system has already shaped decades of future income. This friendly guide explains Switzerland’s three pillars (and the crucial fourth one you build yourself) so you can make smarter decisions long before it’s too late.

From 2025, Switzerland’s Pillar 3a gets a powerful upgrade: you’ll be able to make retroactive “buy-in” contributions for up to 10 missed years — and still get the full tax deduction. Learn how the new buy-in rules work — and who benefits most.

Pillar 2 buy-ins and Pillar 3a contributions both cut your taxes — but they work in very different ways. This guide breaks it down in plain language, with real CHF 50 000 examples and a simple framework for choosing the best strategy for your horizon. If you’ve ever wondered where your next saved franc should go, this is the clearest answer you’ll find.

Most people in Switzerland use Pillar 3a — but many set it up in a way that quietly costs them thousands in lost returns and unnecessary taxes. Here are the five most common mistakes people make with their 3a, and the simple steps that can help you save more and build long-term wealth.