I thought everyone already knew about Revolut, but last week I was having lunch with a friend and realised she had never even heard of it. That made me decide to write about a solution that has saved me thousands of francs over the years, especially now that the summer holiday season is approaching.

What is the biggest problem when paying by card abroad?

The cost.

More specifically, the cost of currency conversion and additional fees, such as cash withdrawal charges at ATMs.

Let’s look at our hotel bill in Greece from last year. At check-out we were asked to pay EUR 10,000. (The number is artificially high because I wanted to use a nice round figure that is easy to calculate.)

We paid with Revolut.

If I had paid that bill with a Swiss bank credit card, there would usually have been two separate costs:

- Exchange-rate spread (the bank gives you a worse EUR/CHF exchange rate than the market rate)

- Foreign transaction fee (often around 1.5%–2.5%)

So let’s compare:

Table 1. Revolut vs Swiss Bank Cards: How Much Money Can You Save?

| Payment Method | FX Rate | FX Fee | CHF Cost |

|---|---|---|---|

| Revolut | 0.9350 | — | CHF 9,350 |

| Swiss bank card | 0.9537 | 2% | CHF 9,727 |

| Difference | CHF 378 |

I still remember when a friend from London came to visit me for a weekend about ten years ago.

She had this distinctive purple card. When she pulled it out to pay for our tickets to the Hürlimann thermal baths, I immediately said:

“No, no, you’ll end up paying much more with your British card.”

She smiled and told me that she wouldn’t.

Interestingly, somewhere between all the chatting and gossiping during our several hours at the spa, this became one of our main topics of conversation. 😊

That purple card turned out to be a Revolut card.

Not long afterwards we were planning a long holiday across several countries with different currencies, so in September 2016 I signed up for Revolut myself.

It was only supposed to be a card for that particular trip.

Yet here I am almost ten years later, still using it.

In fact, I use it so much that it has become my primary payment card for travelling abroad, shopping in online stores I don’t know well, and paying for subscriptions.

The reasons are simple: very low foreign-currency costs, ease of use, security, and extremely clear transaction history. It makes it very easy to keep track of who is charging my card and how much.

The hotel example above is just one of many.

The bottom line is that Revolut was quick to set up and has saved us thousands of francs over the years.

Want to know more?

Keep reading.

If you’d rather skip the article and simply find out whether Revolut is right for you, here’s my checklist.

You should get Revolut if:

✅ You travel outside Switzerland

✅ You pay in EUR, USD, etc or transfer money to family abroad

✅ You shop online

✅ You have Netflix, Disney+, Spotify or AI subscriptions

✅ You invest in US ETFs or in other foreign investments

You probably don’t need Revolut if:

❌ You never leave Switzerland

❌ You only spend CHF

❌ You already have a low-cost foreign-currency card and never shop online

Revolut now has more than 1 million users in Switzerland and over 75 million worldwide.

If you live in Switzerland and occasionally pay in euros, dollars or other foreign currencies, a free Revolut account could save you a significant amount of money on exchange fees.

Even if you only use it a few times a year during holidays, you could still save tens or even hundreds of francs on currency conversion and foreign transaction charges.

Opening a Revolut account costs nothing.

You can keep your existing Swiss bank account exactly as it is.

If you set it up now, you should still receive your card before your summer holiday.

For full transparency: this is an affiliate link. If you sign up for Revolut through my referral link, I receive a small commission for introducing a new customer to them.

TL;DR – For Those Who Don’t Like Reading Long Articles

I rarely describe something as the best, but honestly, it’s hard to find a better multi-currency card than Revolut. It’s free, very easy to use, and excellent for spending abroad, online shopping, and international transfers.

I also use it for all my subscriptions and for shopping on websites I don’t completely trust. Thanks to virtual cards and detailed spending controls, I feel much more secure.

I’ve been using Revolut for almost 10 years. However, I’ve never used it as my main bank account.

In my opinion, for someone living in Switzerland, Revolut works best as a secondary card for travel, foreign-currency spending, and online purchases. I still think it’s worth keeping your main account with a Swiss bank for your salary, taxes, TWINT, eBill, and other everyday banking needs.

For me, the only real drawback is that customer deposits are held with a Lithuanian bank and protected under the Lithuanian deposit guarantee scheme. That’s why I only keep as much money there as I expect to spend in the near future.

How Does Revolut Work in Switzerland?

Revolut was founded in 2015 as a British fintech company. It was one of many startups promising to revolutionise financial services, but also one of the very few that actually succeeded.

Its core product is a multi-currency card that allows you to spend around the world using very competitive exchange rates. The card is linked to the Revolut app, which gives you access to:

- A free CHF account.

- A free Euro IBAN account.

- Sub-accounts in dozens of currencies.

- International money transfers.

Everything is managed through the Revolut mobile app. Besides currency exchange, it allows you to manage your cards, track spending, and access additional services such as travel insurance and investing.

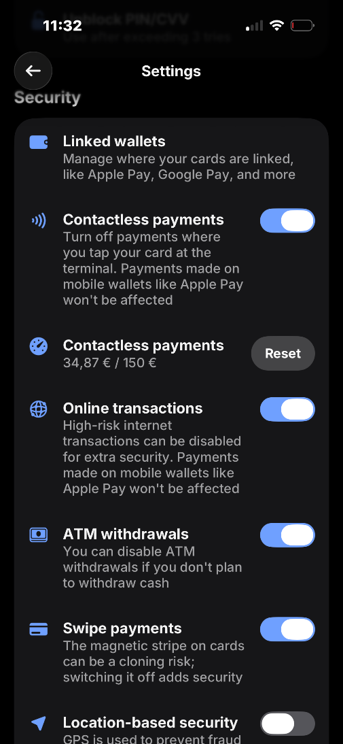

What I personally like most about Revolut is its approach to security. With a single tap, I can freeze or unfreeze my card, disable online payments, disable contactless payments, or set spending limits.

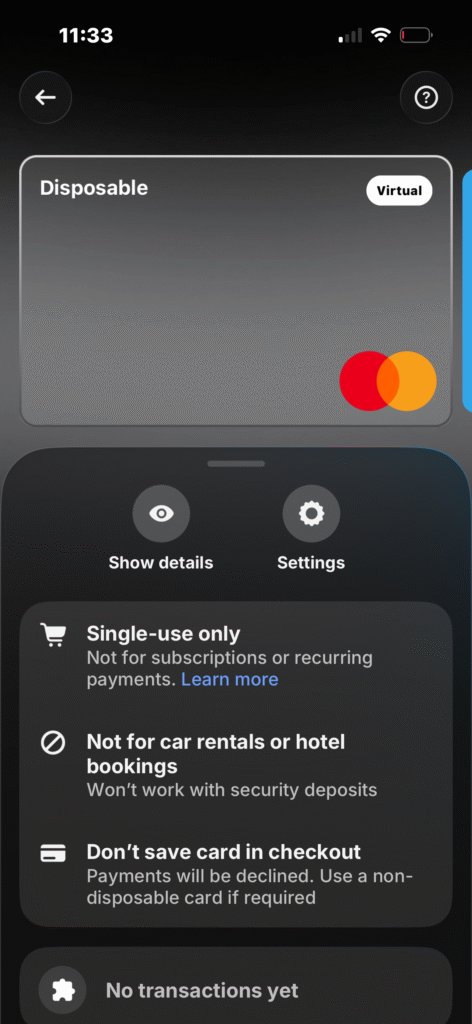

Revolut also offers free virtual cards for online shopping. If a card number is ever compromised, you can delete it instantly and create a new one. There are even disposable virtual cards whose number changes automatically after every transaction.

I’ve been using the free Standard plan for almost 10 years, and it has always been more than enough for my needs.

In this article, however, I’ll focus mainly on Revolut as a travel and multi-currency card. My husband is also a big fan of Revolut and uses the Premium plan, so I’ll share some thoughts on that as well.

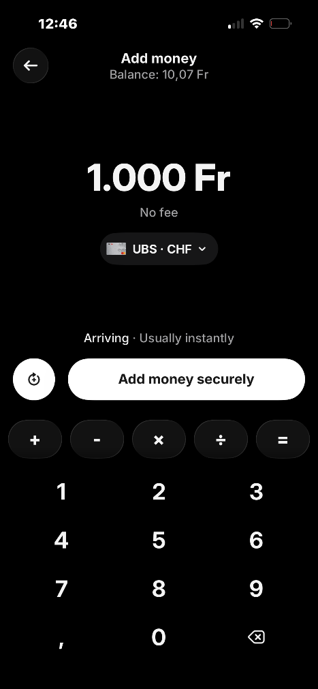

How to Top Up Revolut and Exchange Currency

A Revolut card works much like a normal debit card – you first add money to your account and then spend those funds using the card.

There are two ways to top up your account:

- By adding your bank card details and topping up your account with a chosen amount. The money appears almost instantly. This is the method I use nearly all the time. Since 2025, top-ups with Swiss bank cards have been free once you complete the additional verification process (“beneficial owner”).

- By making a bank transfer from your regular bank account to Revolut. In my experience, the money usually arrives within one working day.

Once you have CHF in your Revolut account, you can start spending straight away. Revolut automatically converts your francs into the currency needed for the transaction, usually at a very competitive exchange rate.

This is particularly useful when travelling. When you pay with a traditional Swiss bank card, you often lose money twice: first through a less favourable exchange rate, and second through a foreign transaction fee. On larger purchases, such as hotels, the difference can easily be CHF 100–200.

Important: the best exchange rates are available on weekdays. At weekends, Revolut adds a small markup (typically around 0.5%) because the foreign exchange market is closed.

Revolut Standard Plan: Limits, Fees and What You Get for Free

The free Revolut plan does come with a few limits:

- Free cash withdrawals up to CHF 200 per month (maximum 5 withdrawals)

- Free currency exchange Monday to Friday up to CHF 1’250 per month

- 1% fee on currency exchanges made at weekends

You can see the current paid plans and their benefits on the Revolut website.

My Personal Revolut Setup for Travel and Online Shopping

At the time of writing, this is how I use Revolut:

- Revolut has become my main card for spending abroad.

- I top up the account only when I need money. (Automatic top-ups are available, but I don’t use them.)

- I pay for subscriptions with Revolut – Netflix, AI tools, and similar services.

- Revolut has also become my main card for online shopping because of the additional security features. I use it for Amazon and many other online stores.

- One extra way I use Revolut: I often convert CHF into USD or EUR in Revolut before sending money to my brokerage account or crypto exchange. In my experience, the exchange rate is much better than converting directly within the investment platforms.

If you’re curious about my brokerage set up, I have been building my portfolio on Degiro for years, but as part of optimizing my capital allocation in Switzerland, I have recently started testing Interactive Brokers. If, after running your own analysis, you have concluded that this is the right next step for your finances, I invite you to open your account using this link. By doing so, you may receive a free IBKR welcome stock bonus, while helping to support my blog at no extra cost to you.

What I Still Use My Swiss Bank Account and Credit Card For

- Salary payments

- Taxes

- Mortgage payments

- Savings

I hope this article has answered most of the questions you may have about Revolut.

If you have any additional questions, feel free to leave them in the comments.

And ff you’re trying to optimise your finances in Switzerland, this card is only one small piece of the puzzle. The biggest savings usually come from taxes, pensions and investing. You can find more of these topics on my blog:

The Swiss Pension System Explained: What You Need to Know Before It’s Too Late

A Proven Way to Repay Your Mortgage – How to Become Debt-Free in Switzerland

How to Choose Your Health Insurance (and Actually Pay Less)

The Best Investment in 2026: 10 Books on Money and Better Decisions

Revolut Switzerland FAQ

1. How to Open a Revolut Account in Switzerland?

Signing up for Revolut can be done entirely through your mobile phone.

The process looks like this:

- Click the link and enter your mobile phone number on the page. Going through the referral page is necessary if you want to receive your card under the current promotion.

- You’ll receive a link on your phone to download the Revolut app. Download it, as the entire registration process and day-to-day account management take place within the app.

- Follow the registration steps in the app:

- Enter your phone number.

- Create a PIN for logging in (you can also use fingerprint or face recognition on supported devices).

- Enter the verification code received by SMS.

- Fill in your name, date of birth, postal address and email address.

- Top up your Revolut account with at least CHF 15. The easiest way is to use a bank card. You can immediately spend this money, withdraw it from an ATM, or even transfer it back to your bank account if you wish.

- Verify your identity by uploading a photo of an identity document (passport, ID card or driving licence) and taking a selfie. This is usually the step that makes people most uncomfortable, as you’re sending photos of official documents. However, it is a standard requirement and is currently necessary if you want access to free Swiss card top-ups.

- Once your verification is complete, you can order both a physical card and virtual cards. In my experience, the physical card usually arrives within about a week.

2. How to Use Revolut Without Paying Extra Fees?

To finish, here are the most important tips I’ve learned from using Revolut over the years:

1. Exchange currencies on weekdays whenever possible

This is when you get the best exchange rates and avoid the weekend markup.

2. Weekend spending is still free if you’ve exchanged money in advance

If you’ve already converted CHF into the local currency before the weekend, payments will simply be deducted from that currency balance. No additional currency conversion is needed.

3. Always choose the local currency

If a payment terminal or ATM asks which currency you want to use, always select the local currency of the country you’re in.

For example, in Greece choose EUR, in Poland choose PLN, and in the United States choose USD.

If you choose CHF instead, the merchant or ATM may apply its own exchange rate, which is usually much worse. This is known as Dynamic Currency Conversion (DCC), and it’s something you generally want to avoid.

3. What Are Revolut Disadvantages and Things to Watch Out For?

It’s worth remembering that Revolut isn’t perfect.

For example, there are still situations where a Revolut card may not work as smoothly as a traditional credit card, especially when a security deposit is required, such as at some car rental companies.

That’s why I always recommend carrying a second card with you when travelling.

Even if you don’t need Revolut today, having it already set up means you’ll be ready for your next holiday or online purchase in a foreign currency.

Top-ups with Swiss cards are currently free after completing verification, although Revolut could change this policy in the future.

4. Is Revolut Safe for Swiss customers? Deposit Protection Explained

To be honest, this is the area where I’ve always had some reservations.

Revolut started in 2015 as a British fintech company. In 2018, it obtained a European banking licence, and today customer deposits are held by Revolut Bank UAB in Lithuania.

For Swiss customers, Revolut now provides a local CHF account with a Swiss IBAN, which makes transfers and account top-ups much easier. However, this doesn’t change the fact that deposit protection falls under the Lithuanian deposit guarantee scheme, which protects eligible deposits up to the equivalent of EUR 100’000 per customer.

Personally, I still follow a “trust, but verify” approach.

I only keep as much money in Revolut as I expect to spend in the near future. If I need to make a larger payment, I simply top up the account shortly beforehand.

When it comes to the security of transactions and cards themselves, however, I have no concerns at all. Have a look at the settings you can change with just one click. That’s why i love Revolut for abroad and online transactions – I have full control of security settings.

In fact, I would argue that Revolut offers more security controls than most traditional banks. Features such as instant card freezing, spending limits, virtual cards and disposable virtual cards give you a level of control that many conventional banking apps still don’t offer.

Join 1'400+ readers making smarter Swiss financial decisions:

Send me the next guide